Which is better: JD.com, Alibaba or Meituan? | Kelvestor

Previously, we discussed about the merits of an “Online Marketplace” business model. If you have not read the previous article, do read it here before you proceed with this article.

What I will be covering today:

- What is the Direct Sales (1P) business model? How does it relate to the online marketplace?

- Comparison between JD.com, Meituan Dianping and Alibaba

- Key Takeaways

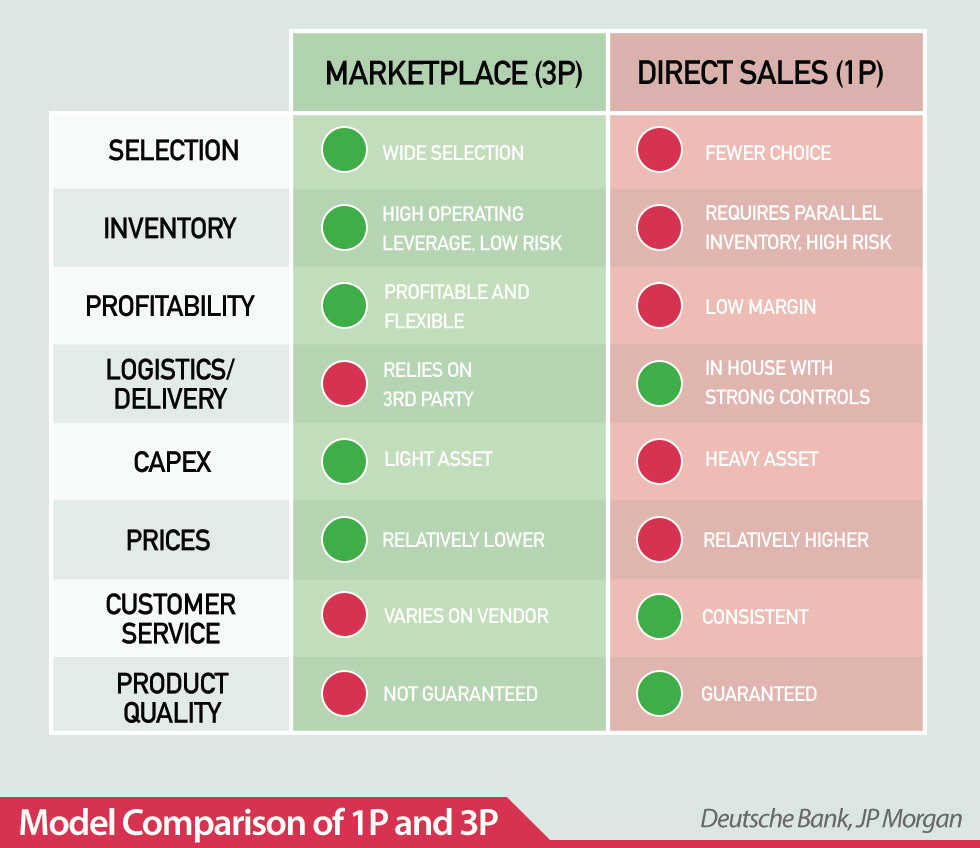

Today, I want to introduce to you another concept called Direct Sales (1P). It’s different from a marketplace (3P).

An example of a business that utilises 1P model is JD.com.

JD.com purchases products from thousands of suppliers such as Haier, stores the items in its warehouse, then sells to its customers with a small mark-up directly via their own logistics.

On the surface, JD.com looks like a terrible business because of the huge capital requirement to run its logistics network.

However, it offers full control over the last-mile delivery experience.

In the case of Meituan or Alibaba (3P model), it might be harder to exert control over the quality of products delivered by its merchants.

On the other hand, JD controls the authenticity of its products sold and delivery time.

Using the table below, it highlights the differences between 3P and 1P:

Now, let’s move on to compare the business models of JD.com and Meituan Dianping.

The Business Model of JD.com

JD.com is one of China’s largest online retailers, clocking US$82.9 billion of sales in FY2019.

They chose to replicate Costco’s playbook by focusing on obtaining scale first before profitability.

Why is scale so important?

Scale provides a buyer with bargaining power to lower the purchasing price.

Part of JD’s playbook is detailed below:

When

JD’s customers buy more from JD 🡪 JD is able to buy more from its

suppliers 🡪 wrestle for cheaper purchasing price from its suppliers 🡪

pass down the cost savings to customers 🡪 JD’s customers get more value

🡪 repeat

It forms a virtuous flywheel effect.

You see, at the start, when JD is purchasing items from their suppliers, they are unable to negotiate for lower prices unless they buy more items.

To combat that, they need to gain scale.

One of the ways is to mark up their products less in order to provide the best value to their customers. As a result, customers buy a larger quantity over time.

Over time, JD’s suppliers are willing to drop their per unit price for them because they have a larger volume. Their purchasing volume also compensates for their decline in profitability.

This is why once JD has scale, they are able to negotiate for lower prices from their suppliers – such that no other competitors can get the same price as them. This allows them to be a cut above the rest.

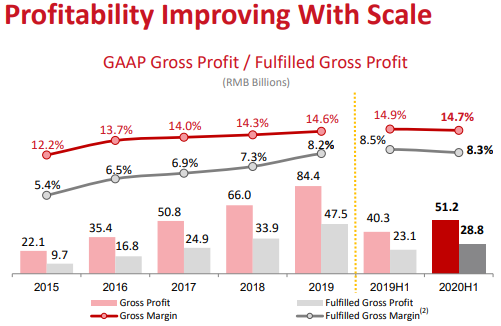

As you can see, this is their gross profit margin over time:

From FY2015 to H1 2020, JD’s gross margins increased gradually.

From my perspective, I suspect their margins could have increased more. However, JD opted to pass on the costs savings by lowering their product prices.

The question remains – is JD’s business model is terrible or are the gross margins are intentional?

My belief is that the gross margins are intentional.

JD kept passing on cost savings to their customers to drive their scale strategy. This has the added perk of adding huge customer satisfaction, which may drive word-of-mouth marketing to increase the number of users on their platform.

However, in the pursuit of offering quality and authentic products, JD does not enjoy an asset light business model and their profitability is lower.

On this point, this does not mean that JD has a lousier business model.

On the flipside, JD enjoys something called “free float”.

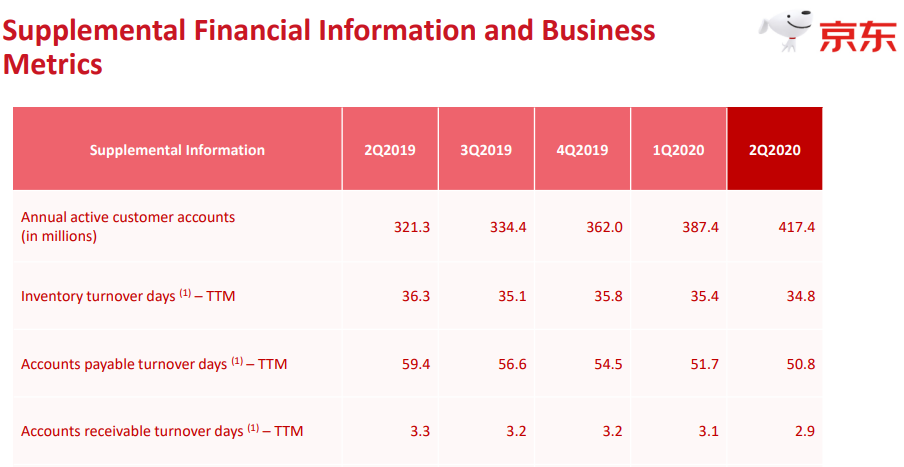

Looking at this table below:

JD’s inventory needs 34.8 days to be sold and 2.9 days for sales money to be collected, then they have 50.8 days before its suppliers asks them for their money.

34.8 days + 2.9 days – 50.8 days = negative 13.8 days. This means that JD has a negative cash conversion cycle and thus could use the money to invest in its logistics needs in the short period for free.

JD has invested in its logistics heavily since day 1 and is the best logistics provider in the whole of China.

During the past few months of COVID-19, JD was able to utilise this strength to send their goods to its customers, whereas other platforms like Taobao (who utilise third party logistics) ran into shipment issues.

Now that we have covered JD’s business model. let’s look at another app giant in China with a different business model.

The Business Model of Meituan Dianping & Alibaba

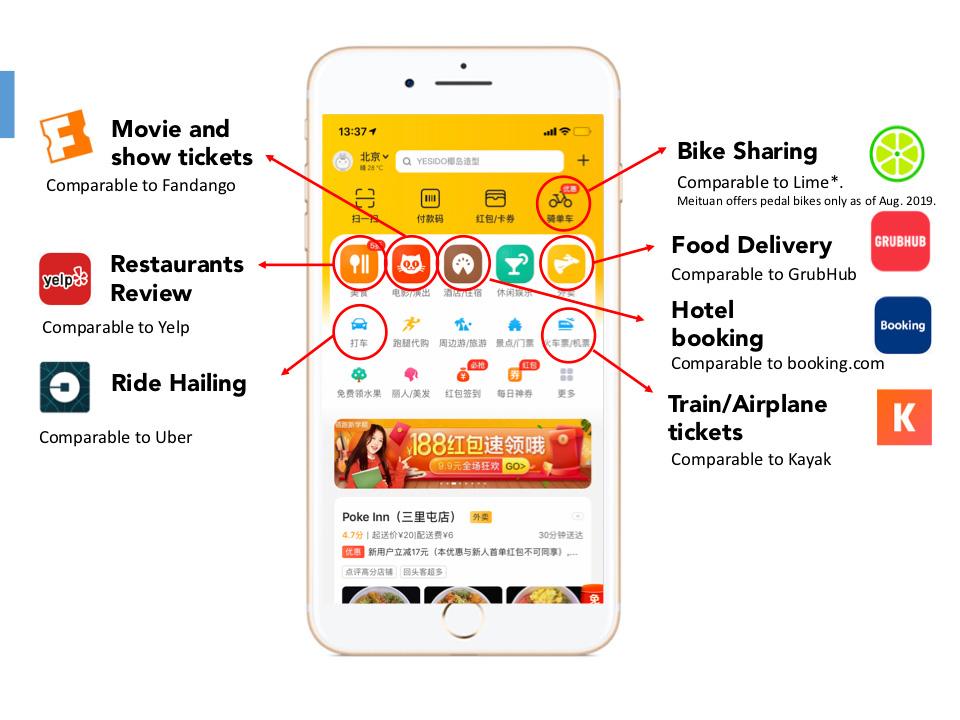

Meituan is a great example of the 3P model. Alibaba, just like Meituan, is also on the 3P model. Today, I will cover more about Meituan because it is a slightly less talked about (but equally amazing) company.

Although less known overseas, it is actually a super-app that everyone in China’s top tier cities would recognise. It is a service marketplace that offers travel booking, movie tickets, ride hailing, home rentals and food delivery services.

The business is extremely light and scalable except for heavy capital requirements on logistics to support their food delivery business.

However, they also chose to dominate the food delivery business because it is easy to acquire customers very quickly. This is because the usage frequency of this app is extremely high – an average Chinese also opens the Meituan app more than 3 times per day.

For example, for most of the busy Chinese salarymen, they often value their working time above the cost of food delivery. As such, they would gladly pay Meituan to deliver their meals to their offices.

To dominate this space, Meituan understands the need to control the last mile delivery and this is why Meituan has its own food delivery fleet.

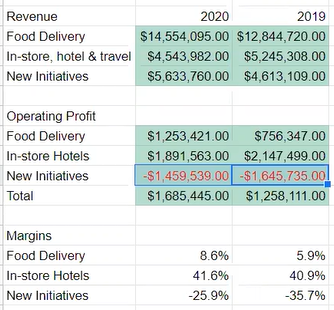

Looking at Meituan’s business segments, you will notice a few observations:

As you can see, food delivery business has the lowest margin but is responsible for growing the number of users on the platform quickly.

On a daily basis, consumers buy food more often than booking hotels.

But by having those users on their platform, Meituan is able to cross-sell other services such as hotels to the same group of users.

This is especially important because, unlike its food delivery business, Meituan is merely earning a commission cut from the hotels and not providing the hotel experience. This is why the hotels segment has a high profit margins.

The ability to cross-sell is what makes a superapp successful.

It is able to earn more money without incurring any incremental expenses. There is no double spending of customer acquisition cost for a customer who utilises two services out of the superapp.

That being said, a marketplace is extremely vulnerable when it is trying to scale its first segment.

It is the common phase where the cash burn is the highest, customer acquisition is at all-time high and scale is needed to breakeven on upfront investments.

Previously, when Meituan was scaling its food delivery business, it had to raise funds on multiple occasions. At that point, some investors were feeling nervous that Meituan would run out of money.

Confidence was restored when the first segment became profitable. Then, utilising the profits from the food delivery business, Meituan entered into the hotel booking service aggressively.

Now, since the food delivery business and hotels are profitable for Meituan, the most profitable thing for them would be to re-invest their profits to enter new verticals such as groceries.

This is exactly the playbook of online marketplace / platforms business model.

Build a profitable segment and reinvest the profits, and repeat the process with each segment becoming profitable.

With each segment, it also attracts a new group of users.

For example, there are different groups of people who download Meituan app for many different reasons.

Some download it because of the food delivery service, while some download it for the hotel booking service.

Key Takeaways about Marketplace Business Model

- Access to financing and reducing cash burn are extremely important in an early stage of a market place business model.

- Meituan was seen as a riskier business because they had to raise a huge amount of capital to get its Food Delivery business off the ground and to offset the initial cash burn when entering into a more profitable segment of hotels.

- On the other hand, JD had no issues like Meituan’s in its early days because its suppliers indirectly financed their entire growth by extending generous payment terms.

- But now, it seems apparent that Meituan has a better business model.

- A marketplace business model is scalable and it does not require huge capital to grow.

- However, the key differentiator of a successful one is whether the users are frequently using the app. Frequency of usage builds habits.

- Meituan would not be as successful if they entered into the hotel category first, because they would not be able to build such a big customer base.

- Once the habits are created, it is likely that people will use the app a lot more frequently.

Year till date, JD.com and Meituan rose by 114% and 152% respectively.

At the end of the day, understanding the challenges and growth potential of each model provides you with the superior skill to invest in the most well-positioned player in this industry.

See the difference in share price performance between JD.com and Meituan? I’m not exaggerating when I say you could even pull ahead your goal of being financially free by years.

The rise of marketplaces is just beginning. You’re either going to miss out on it or you’re going to ride the growth curve.

Stay tuned while I launch the next series! I will discuss other aspects of marketplace business models using two new examples!

I hope my article has benefitted you. If it has, please pay it forward by sharing it with more people!

https://kelvestor.com/blog/which-is-better-jd-com-alibaba-or-meituan/