My telegram channel : https://t.me/ltachannel

My blog : http://bursalogicanalysis.blogspot.my

Simply due to N2N highly potential to become next JFTECH, which can Meletup from RM 0.80 all the way to RM 2.29 within just a few month time, therefore we further share our LTA views in this company.

My blog : http://bursalogicanalysis.blogspot.my

Simply due to N2N highly potential to become next JFTECH, which can Meletup from RM 0.80 all the way to RM 2.29 within just a few month time, therefore we further share our LTA views in this company.

It's so less chance to find a great profitability stock that can

easily estimate and with very strong business background, therefore I

have to write one more post to share my views and hope it can be same

like JFTECH again!

You can find out why I like N2N on previous post at link below:

This post we will only discuss about N2N fundamentals like balance sheet, quarterly result, business details and futures prospect.

Let us study the latest quarter result first.

Looking at the latest quarterly result balance sheet,

Total cash = Deposit with Licensed Bank RM 94 million + Cash at Bank RM 38 millions

= RM 132 millions !

Total loan = Long term loan RM 74 millions + short term loan RM 2 million

= RM 76 millions

Total cash - Total loan = RM 132 million - RM 76 million = RM 56 millions

Total share issued 477 millions / RM 56 million = RM 0.117 nett cash per share.

As long as the company is nett cash, usually it deserve higher valuation !

How about cash flow is it positive?

Very positive !!

Again we read this quarterly result and to see how much potential it should be for the next few coming quarter:

We can see the obvious jump in Revenue and net profit, you should already know it's due to newly acquired company name AFE Solution Ltd which have most business in Hong Kong. To know whether how much it contributes, we can check from latest report as well:

We can see May result still not yet include new acquired company's contribution.

We can see obviously compare with May's quarterly result which not yet show any contribution from Hong Kong, Macau and Vietnam but in latest August quarterly result, it show the contribution from this 3 country increase extra 240 % revenue, which DOUBLE UP the revenue and also it's profit !

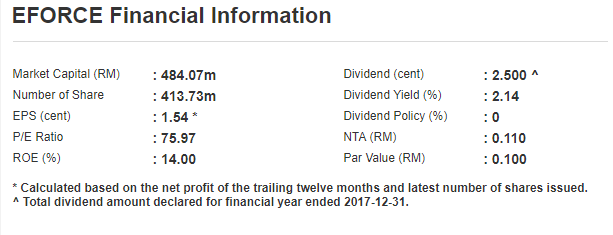

Let's also compare N2N direct competitor EFORCE which also provided trading solution in Malaysia.

I don't dare to compare at all !

If compare N2N price should limit up at least 3 time !! ?

EPS 4.02 x PE 75 (EFORCE current's PE) = RM 3.015 !!

N2N EPS is 2.6x times higher compare to EFORCE and yet to calculate if N2N continue to post better result then EPS might be even higher !

If look at N2N PE which is almost 3.4x times lower to EFORCE !!

NTA of N2N also almost 4 time higher compare to EFORCE !!

And yet EFORCE stock price at RM 1.10+ and N2N only RM 0.80+ ??

Since we know that the contribution from newly acquired company

contribute a lot, we can roughly estimate upcoming quarterly result

revenue and profit as below to project how much N2N should worth:

First quarter net profit : RM 3.624 millions = 0.77 EPS

Second quarter net profit : RM 9.944 millions = 2.12 EPS

From here, we have to estimate the future already !

We use very low profit of RM 5.00 million will do. If doing better, it's going to greatly impact the PE and stock price.

Third quarter net profit estimate : RM 5.00 mil = EPS 1.04

Fourth quarter net profit estimate : RM 5.00 mil = EPS 1.04

Total EPS = 0.77+2.12+1.04+1.04 = EPS 4.97 in RM its RM 0.0497 per share.

RM 0.0497 it's about PE 21 if based on RM 1.05.

However if coming two quarter able to deliver better than just RM 5.00

million net profit (should be can since last quarter already RM 9

million), it's expect to much lower down the PE value !

(for example if Q3, Q4 post RM 7.5 mil, total EPS = RM 0.0157. Price RM 1.05/EPS 0.0603=PE 17 only.)

If earning maintain around RM 9.0 mil, then the price definitely SUPER Big Meletup Up !!

I can

tell you why it worth more than just PE 20 as this is a very strong

growth stock with nett cash position and strong market leader position

which ensure their business and profitability and capabilities !

In Malaysia we should know that only one Competitor which is EFORCE. N2N have a long list of client too, and most importantly all these client very unlikely going to switch to other trading solution as it going to spend a lot of cost therefore N2N business is very solid and steady:

-------EXCHANGES business-------

1)Aseambankers

2)CIMB Bank

3)Citibank

4)Maybank

5)AmFraser

6)AmSecurities

7)Apex Securities

8)CIMB Securities

9)HWANGDBS

10)Kenanga Investment Bank Berhad

11)PM Securities

12)SJ Securities

13)Macquarie

14)AffinTrade

15)TA Securities

2)CIMB Bank

3)Citibank

4)Maybank

5)AmFraser

6)AmSecurities

7)Apex Securities

8)CIMB Securities

9)HWANGDBS

10)Kenanga Investment Bank Berhad

11)PM Securities

12)SJ Securities

13)Macquarie

14)AffinTrade

15)TA Securities

http://bursalogicanalysis.blogspot.my