Since

1930, dividend has been responsible for 42% (on S&P 500) of the

stock market return so there’s little surprise that it is one of the

main criteria we look for when picking stocks. However, in

investing, everything involves an opportunity cost. So the question to

ask is - Is focusing on dividend as a key selection criterion the right strategy for me?

Before

you decide if it is the right strategy, first we have to understand

what it is. Let’s think about a bathtub system. In a bathtub system, you

have water flowing in from the tap into the tub with some retain in the

tub (or stock) while the rest flows out through the sinkhole.

When you apply this to business, what do the inflows represent? It’s the earnings. Or more precisely, the return on capital (ROC) for the business. The higher the ROC, the bigger the inflows. Once the water flows into the tub, the management will ask “How much should we reinvest to grow the business and how much should be paid to our shareholders?” The amount of dividend that is paid out is the outflows. And for every dollar paid out to shareholders, there will be one less dollar retained to grow the business.

That

is the big picture. Dividend and growth come from the same pie (or the

same tap). You cannot have both at the same time. It doesn’t matter how

you cut or slice the pie, if the size of the pie doesn’t change, doing

more of one thing means less of the other. If a company pays out a

majority of their inflows as dividend, the future growth rate will be

low. Whereas if a company wants to focus more on growth, they either

have to 1) Reduce dividend or 2) Improve ROC.

So

that’s the opportunity cost. If your focus is on dividend stocks, there

will be less capital for these type of companies to compound future

growth for you. The same analogy can be applied to personal finance. If

you consume more of your savings today, there will be less for future

wealth. A dividend is a form of consumption. Yes, there are disciplined

investors that reinvest all their dividend but more often than not, most

dividends are being consumed unknowingly rather than reinvested. A

dollar of dividend that is not reinvested will lower your long term

compounding power. It is like a car always on the 1st gear going up the

hill. Here is an example.

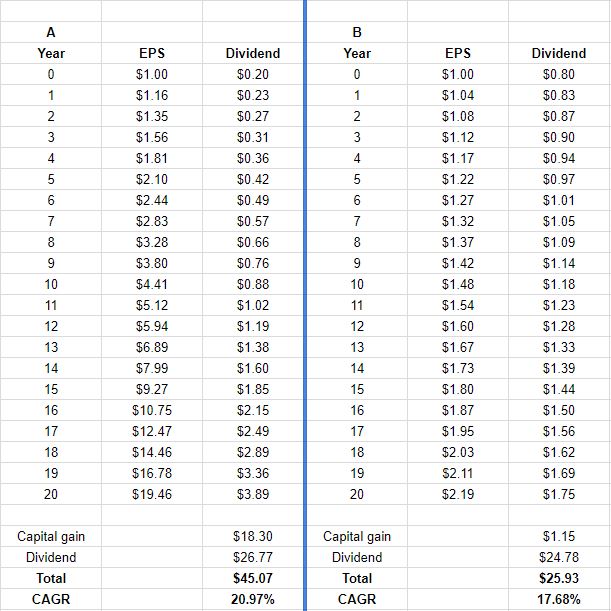

Both

stocks, A and B have a ROC of 20%. Stock B is a dividend stock, paying

out 80% of their earnings and reinvest the remaining 20% for 4% growth

(Growth rate = ROC*Reinvestment rate) due to lack of opportunities.

Whereas stock A is a compounder. It is a small fish in a big pond and

given there are many opportunities out there, it can grow at 16%

(reinvesting 80%) and payout a conservative 20%.

You

would notice there’s a slight difference between both CAGR figures.

Stock B has a lower CAGR because the dividends are not reinvested. The

difference of around 3% doesn’t sound much, but on a dollar level, stock

A’s return is 80% higher than B after 20 years. Instead of $45 vs. $25,

think $450k vs. $250k, or $45 mil vs. $25 mil. Dividend that is not

reinvested might not amount to many each year year, but over the

long-term, it becomes exponential.

When

a company pays out a majority of their earnings, the weight shifted

from the management to the shareholders. If dividend is to be

reinvested, shareholders have to do the heavy lifting by finding similar

or better opportunities in the market. Sometimes, the timing of

dividend doesn’t always coincide with opportunities in the market, and

at times, runs in opposite direction. In a bull market, there will be

fewer opportunities as better earnings leads to higher dividend and

share price gets bid up in the process. The opposite applies in a bear

market. Shareholders also need to consider the time required to research

and find these opportunities because time is an opportunity cost. And

when time constraint and limited opportunities collide, there’s a

tendency to make rash decisions that lead to bad investments. These are

subtle risks that are less discussed when reinvesting your dividend but

are nonetheless real.

On

the flip side, dividend can be a better choice in some cases. If it is

the main source of income for an investor or if a company has limited

growth opportunities; poor allocation skills that lead to

diworsification; face highly uncertain future prospect or destroys

shareholders value by opting for growth that has a poor return, it makes

sense to focus on dividend over growth.

For

investors where dividend income is optional and can afford to wait

10-20 years, you can fully exploit this edge. The best way to do so is

to leverage on stocks that can redeploy most of their incremental

earnings at a very high rate for a long period of time - the

compounders. As the example shows, 2 stocks can have the same ROC (and

same cost of capital) but that doesn’t give you the full picture. The

one that can grow faster is going to be more valuable. Make no mistake,

compounders are the rare breed. Most companies cannot continue to

maintain a high ROC for a long time or if they succeed, size will

eventually prevent them from reinvesting all their capital. With that

said, it is good to keep in mind compounders should always be the one

you are looking for, especially during a crisis.

For

dividend investors, dividend will continue to play an important role in

determining long term return. The keyword is ‘long-term’. If you

remember the bathtub system, it is worth the time to pay more attention

and ask “How sustainable is the ROC in the long run?” rather than “What

is the current dividend yield?” because when the ROC gets eroded by

competitions, dividend will soon follow.

If you find this helpful, share it, subscribe and learn to be a better investor.

http://klse.i3investor.com/blogs/JTYeo/128478.jsp