ESAFE (0190) - Eversafe Rubber IPO: 5 Things You Need to Know

A company set to be listed on 21 April 2017 is Eversafe Rubber Berhad.

Here is a quick guide to bring you through this rubber-products maker!

1. Eversafe’s Profile

Eversafe Rubber deals with the development, manufacturing and

distribution of tyre retreading materials, as well as tyre retreading

operations. Its tyre retreading operations are carried out by its

subsidiary, Olympic Retreads.

In 2015, its market share for rubber compounds and tyre retreading in

Malaysia stood at 22% and 4% respectively. Its customers mainly comprise

of tyre retailers and fleet operators, and are primarily concentrated

in the northern region of Peninsular Malaysia.

2. IPO Details & Usage of Proceeds

The company plans to issue a total of 48 million new shares at 36 sens

each. 12.5 million will be allocated to the Malaysian public, 11.5

million shares will be allocated to its directors and the remaining 24

million shares will be placed out to institutional and selected

investors.

The shareholders of Eversafe Rubber would also offer up to 30 million

existing shares for sale, with 24 million shares placed out to approved

Bumiputera investors.

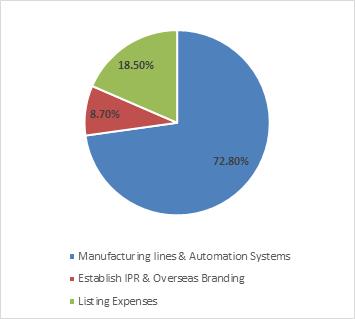

Eversafe Rubber Bhd plans to raise RM17.28milion from its IPO with a breakdown below:

- RM12.6 million (almost 73%) will be allocated to its new manufacturing lines and enhanced automation systems.

- RM1.5 million will be used for the establishment of its intellectual property rights and overseas branding initiative

- Remaining RM3.18 million going to listing expenses (a hefty 18.4% compared to what they getting from the IPO funds).

The funds will be utilized over a timeframe within the next 2-3 years. The proportion is graphed below for your easy reference.

3. Financial Health

According to the P&L statement derived from its prospectus, its

revenue has been fluctuating from year FY2013 to FY2015; same goes to

its net profits. However, what is worth noting is that the revenue and

profits doesn’t go hand in hand. Take for example FY2014, revenue is the

highest among the 3 years but net profits came out to be the lowest.

This is due to the spike in distribution costs and lack of substantial

‘other operating income’.

Its Earnings per share of 9M2016 came out to 0.031. If annualized, it

becomes 0.041. With that, we can estimate its IPO P/E ratio to be 0.36 /

0.041 = 8.78x. (rather low in our view).

Whereas for its dividend policy, the company intends to pay out between

40% to 60% of its PAT to shareholders in the near future. Based on

FY2016 figures and IPO price of RM0.36, this translate to an estimated dividend yield of 5%.

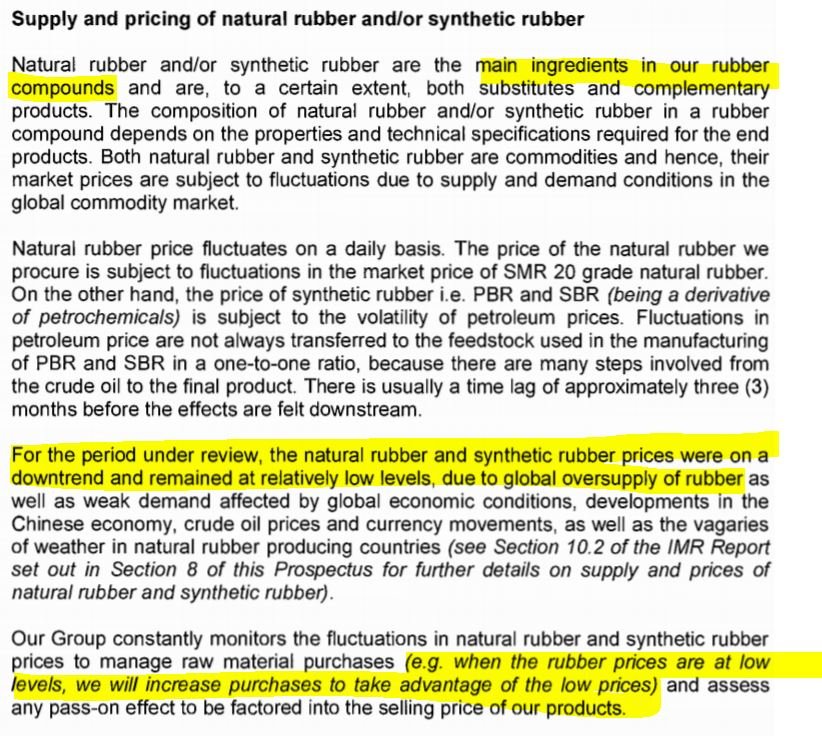

4. One Crucial Risk

As shown above, Eversafe’s operations are highly dependent on rubber

prices as they are the main ingredients in their rubber products.

Furthermore, the recent financials you are seeing are based on

multi-year lows of rubber prices. Thus, it is important to monitor if

the rubber price were to go up and affect the profits of Eversafe

significantly.

5. Growth Prospects

You may have heard of how the company is planning to utilize the IPO

money to develop new manufacturing lines and automation systems to

increase production efficiency, in line with the company’s strategy to

reduce dependency on foreign workers.

Furthermore, the company intends to increase their export sales to new

markets outside the ASEAN region, with a primary focus on Brazil and

other countries in the South American region. You can read more about

it here.

Conclusion

While these growth initiatives are good for the company in future, we

do have some lingering concerns on its industry. It is

highly-competitive for the rubber compounding and tyre retreading

industries.

It is also accompanied by the fact that the company’s import of raw materials is mainly denominated in USD. A continuous fall in Malaysian ringgit will translate to higher costs of input.

ESAFE (0190) - Eversafe Rubber IPO: 5 Things You Need to Know

http://klse.i3investor.com/blogs/small_cap_asia/121065.jsp

There is also this recent news about

how re-treaded tyres are costing road accidents. However, i believe

that it will still continue to have customers due to its low costs

advantage, especially in the transport industry.

Nevertheless, the IPO seems very hot with an over-subscription of amazing 65 times by

the public! Its low P/E ratio of 8.78 times and decent dividend yield

of 5% shows that many people may be willing to take a bite of this

stock.

A final note to all to take note that the IPO listing date is drawing close on 21 April 2017… Huat ah!

Fancy an Ebook that teaches you the hallmarks of multi-bagger stocks

and how to find them? Simply click here to receive your copy of a

brand-new FREEEbook titled – “100 BAGGERS” by Christopher W. Mayer here today!

Last but not least, do remember to Like us on Facebook too as we share the latest investing articles and stock case studies for you!