The Power of High Profit Margin when production is increased

As we can notice from past 9 months results, Annjoo recorded a net profit margin of 9.5% (highest among 4 rebar players). Let see a news that AnnJoo’s CEO said they plan to raise their steel output by 21% in 2018 on higher orders as below:

https://asia.nikkei.com/Markets/Nikkei-Markets/INTERVIEW-Ann-Joo-To-Raise-Steel-Output-21-In-2018-On-Higher-Orders-Managing-Director

Source: Asia.nikkei.com news

Main key message from the above news: Annjoo still has SPARE capacity in their production. They still can increase their produtivity according to orders. In fact, their website shows that they have 1470k metric tons (650k bar + 820k billet rated capacity using EAF) and 500k metric tan using Blast furnace. What make me wonder is the total rated capacity of Annjoo 1970k metric tons is still much higher than 850k metric tons production target (as per Annjoo CEO words in Asia Nikkei) in 2018. (https://www.annjoo.com.my/ann-joo-steel-berhad/)

Before we calculate the possible 2018 profit margin, let us see a price chart of 2H2017 of rebar price from MITI weekly bulletin as below:

Source: Source: MITI_Weekly_Bulletin (July, Aug, Sept, Oct, Nov and Dec)

The average Q4 (Oct, Nov, Dec) steel bar price is around RM2480 based on MITI price.

What I wish to show you is when ASP (average selling price) of rebar is increased, Annjoo profit margin may be expanded as they have high inventory level and their Blast furnance which are more efficient than EAF system.

Based on the 21% of produciton expansion (850k ton from 700k ton) metric tons as per Annjoo’s CEO (Dato Lim) in the Asia Nikkei’s Interview, the estimated increment in Annjoo net profit (GP) in 2018 is given by the below equation:

NP = 2017 Revenue X 1.21 (21% increase in production) X 10.5% (higher PM as ASP increases by 10%)

= RM2240M X 1.21 X 0.105

= RM285M

PM = Profit Margin (asumme increase from 9.5% to 10.5% due to ASP increase more than 10%)

The estimated RM285M profit translated to 52.9 sen EPS.

Estimated NP per quarter = RM71.25M à 13.2 sen EPS

Actually the ASP for past 20 days of Jan 2018 stayed above RM2700 (MITI data). If the price can be sustained above RM2500 in 2018, the profit margin for Annjoo and other rebar players will be further improved.

The estimated net profit shows that when profit margin is higher, overall net profit will be multiplied by a larger factor that lead to higher value of profit. The profit can be even higher especially the revenue/production can also be increased (mean net profit AMPLIFIED by both revenue and profit margin).

Annjoo has a dividend policy of 60% of their profit and their dividend yield is 4.34% based on current price. Based on their highest profit margin among rebar players, its fair target price should be in the range of PE10x to PE12x.

Let have a 10% discount of the 52.9 sen EPS and with PE10X,

Fair value of of Annjoo in 2018 = 52.9 x 0.9 X 10 = RM4.76

Q4’17 profit estimation

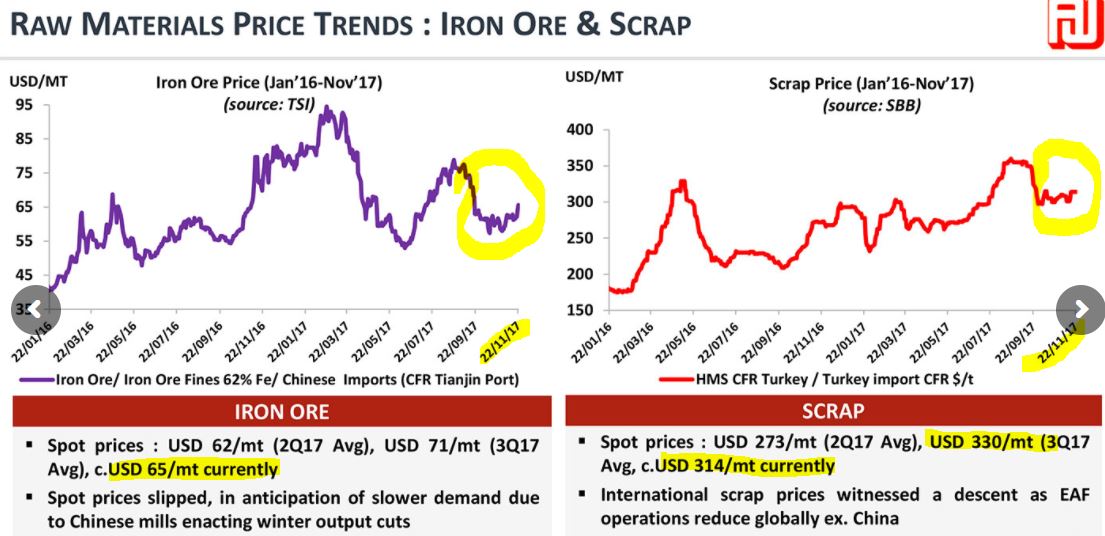

Before we started to estimate the profit Annjoo Q4’17 profit, let us have a look on the Let see the scrap metal and Iron ore price (Annjoo raw materials) as per chart below.

Source: Annjoo corporate presentation slidies

There is about average of 15% price increment in the scrap iron cost but there is some price drop is Iron ore. Remember blast furnace of Annjoo can switch to use cheaper Iron ore when scrap iron price is high. In fact, If we calculate the percentage of increment (RM2100 in July to 2640 in Dec), there is around 25.7% increment in rebar selling price. The price hike their rebar selling price (25.7%) is more than enough to cover the raw material cost increment. THe price till Nov should be enough to cover the Q4 estimated material cost as the order of iron ore or scrap may need to take 1-2 months.

To estimate profit of Annjoo in Q4’17, let us go through the ASP price in Q4 as compared to Q3 as in the table below:

|

2017 |

ASP per ton (RM) |

QoQ comparison |

|

July |

2000-2200 |

Ave = 2100 |

|

Aug |

2200-2550 |

Ave = 2375 |

|

Sept |

2500-2650 |

Ave = 2575 |

|

Oct |

2650-2350 |

Increased by 400 if compared Oct vs July |

|

Nov |

2400-2500 |

Increased by RM75 if compared Nov vs Aug |

|

Dec |

2500-2775 |

Increasde by RM62 if compared Dec vs Sept |

|

ASP |

Q3 = 2350 Q4 = 2480 |

Increase by RM130 if compared Q4 vs Q3 à Increment of 5.5% in Q4 vs Q3. |

Let us calculate the possible profit Q4’2017 table below:

|

Q4 |

Q4 = 2480 |

NP = 68.25mil Based on net profit margin of 10.5% and slightly higher revenue (8% more) of about 650mil. 10.5% (vs 9.5%) profit margin is due to higher ASP in Q4 as compared to Q2, Q3. |

RM68.25 mil profit is equal to EPS of 12.66 sen.

2016 and 2017 Quarter Profit Comparison

|

|

2016 (EPS in sen)

|

2017 (EPS in sen)

|

|

Q1 |

1.10

|

14.77

|

|

Q2 |

18.46

|

5.68

|

|

Q3 |

4.58

|

9.28

|

|

Q4 |

9.18

|

?? estimated about 12.66 sen

|

|

Total |

33.3

|

Estimated ~42.39 sen

|

Local Rebar Demands

The main rebar consumption in Malaysia is from infrastructure projects such as bridge, highway, and piling works of most of the new buildings. Let see a photo for the rebar application in piling process as shown in the photo below.

Source: https://research.engineering.ucdavis.edu/gpa/foundations-deep/pile-group-cap-in-sf/

The mega infrastructure projects awarded in 2017 should provide a good demand for the Rebar companies. These mega infrastructure projects include MRT2, LRT3, Pan Borneo Highway Sarawak, Gemas-JB double tracking .

One of the main infrastructure projects winners is Annjoo which it has the highest profit margin and inventory among 4 rebar listed companies in Malaysia.

Let have a look on Malaysia Mega Construction projects activities overview as below:

Source: Various online newspaper reports

The total contract value for the 12 Mega projects as listed on the bar chart is RM189.9billion (excluding HSR project). Most of the project is just started from 2H 2017 and 2018-2019 is expected to consume a lot rebar for these projects. Just assume 7% of these infra projects is for rebar will lead to RM11.34 billion (11,340 mil) revenue for rebar companies. Most of the Mega infra projects still at their early stage (around 10%-30% of total progress, pls refer to qtr report of Gamuda Dec 2017). As per what I know, the consumption of rebar will be at the highest level (expected to be happened in 2018-2019) for forming the frame/structure of the buildings/bridge/highway (when construction projects enter 15-50%).

From the bar chart above, I can see high profit visibility (due to stronger demand expected in 2018) of Annjoo. The latest average MITI rebar price (on 19 Jan) is still stand at RM2725 per ton as per figure below:

Source: MITI weekly bulletin on 24 January 2018

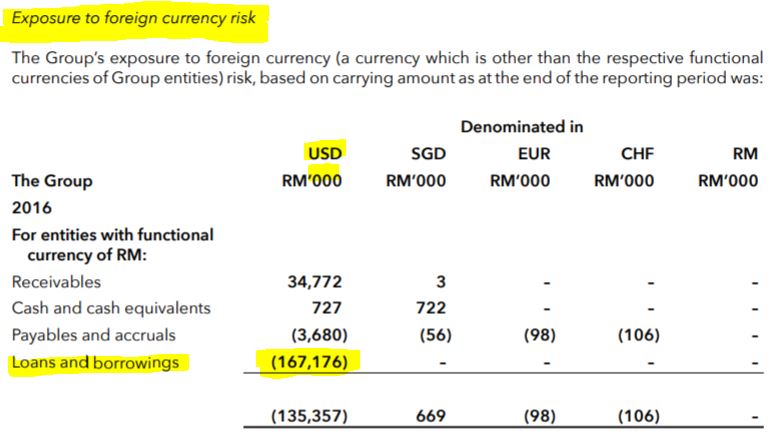

USD Denominated Loan

As per Annjoo 2016 Annual report, Annjoo has about RM167 mil loan is denominated in USD. RM recently has strengthening against USD by more than 10% in 2017 (Dec vs Jan 2017). I expect Annjoo will has some forex gain due to their loan amount in USD will be lower due to strengthening of RM.

Source: Annual Report 2016

Summary

1. Annjoo plan to increase their production from 700k tons to 850 tons in 2018 due to stronger order received since Dec 2017 (refer to Asia Nikkei news).

2. Average selling price (ASP) has increased to RM2480 in Q4’17 and currently the price even higher in Jan 2018 (around RM2700 per ton for the past 20 days). If this price can be sustained, Annjoo likely to earn RM285 mil (EPS of 52 sen) in 2018.

3. The higher ASP in Q4 may produce higher profit (RM68 mil or EPS of 12.66 sen) in Q4 for Annjoo. This implies Annjoo PE may drop to 8.14 after Q4 result is released. Based on current price of RM3.48. There fair forward 3-month PEx is 10-12 (short term tp of RM4.24) which indicates an upside of 23%.

4. Annjoo has the highest inventory (RM800mil+) level among top 4 rebar players and this lead this better opportunity to reap profit in high rebar price in Q4 of 2017 and in 2018.

5. Cash flow generation from operation is strong (more than 50% than accounting profit) from past 9 months of 2017.

6. Annjoo has dividend policy of 60% and the normally they will declare dividend in coming Q4 (based on past years practices).

7. RMUSD rate appreciation (3.93 now) in Jan 2018 which implies that Annjoo stands to have lower import cost for their raw materials and possible to have some forex gain. In fact, the rate of RM has appreciated around 10% (from early Q3 rate of 4.3 to 3.93), this drop make contributes higher profit due to lower material import cost.

8. There should be some forex gain due to lower payable amount in Annjoo’s USD denominated loan.

If you interested on my future analysis reports, please contact me at davidlimtsi3@gmail.com

You can get my latest update on share analysis at Telegram Channel ==> https://t.me/davidshare

Disclaimer:

This writing is based on my own assumptions and estimations. It is

strictly for sharing purpose, not a buy or sell call of the company.

http://klse.i3investor.com/blogs/david_masteel/145300.jsp