I formed two value investing study groups in Seremban a few years ago. All group members were hungry for knowledge. We studied books, cases, and companies intensively. Some of them became my best, if not good, friends. Some remains as acquaintances.

Having undergone that learning process, however, the conversation below emerged whenever the KLSE index or broad market did not seem to be in their favor :

A: John, I am queuing to sell this stock.

Me: Why?

A: Isn't that obvious? Lower (quarterly) earnings (year-on-year) leh.

Me: So?

A: I better take profit than losing my pant.

Me: ... (I paused a second thinking to respond)

A: Sold! Gao dim.

Me: Buy me a meal then. (speechless in my heart instead)

A good read written by Howard Marks suggests that:

- First-level thinking says, "It's a good company; let's buy the stock." Second-level thinking says, "It's a good company, but everyone thinks it's a great company and it's not. So the stock's overrated and overprices; let's sell."

- First-level thinking says, "The outlook calls for low growth and rising inflation. Let's dump our stock" Second-level thinking says, "The outlook stinks, but everyone else is selling in panic. Buy!"

- First-level thinking says, "I think the company's earnings will fall; sell." Second-level thinking says, "I think the company's earnings will fall far less than people expect, and the pleasant surprise will lift the stock; buy."

It seems like my friend 'A' was not alone in promoting the garage sale of Latitud. They sold the stock for an obvious reason - lower y-o-y quarterly earnings.

Blessed by their sell-off, opportunities present themselves for certain quarters to enjoy the garage sale. In particular, through Samarang Asian Prosperity Fund (previously known as Halley Asian Prosperity Fund), Samarang LLP (previously known as Halley Sicav) emerged as one of the ten largest shareholders in October 2017.

After crossing the 5% shareholding line, Samarang reported itself as a substantial shareholder of Latitud in the late Nov 2017.

Just, who is Samarang?

How is Samarang's track record?

The fund, which is rated at the highest level by Morningstar rating house, has so far continued to acquire Latitud shares from the open market. Click on this link to view their recent acquisitions.

As at 15 Dec 17, Samarang has acquired 5.99% of Latitud shares.

What do Samarang see in Latitud? My wild guess...

These trailing valuation metrics are smaller than those of the past 5 years. For example:

- Trailing 6.4x P/E vs 6.5x-8x P/E in the past 5 years

- Trailing 0.71x P/BV vs 0.9x-1.5x P/BV in the past 5 years

Business wise, Latitud is striving to expand its income stream and improve its value chain performance (ie margins) through vertical integration.

I wonder what was the motivation behind the sale. Was it related to (over)valuation, pessimism and/or fear?

Sellers were unlikely to know that Jcbnext was happy to buy over their shares. The company has been inactive in buying back shares until... (you guess?)... the recent months!

The Founder - Mark Chang explained the shares buy back in an interview before Jobstreet was sold. Here is an excerpt.

How's its investment performance, at least, in the short-run?

Shares buy back is activated when the stock price of Jcbnext falls below a threshold.

What could be this threshold?

After disposing Jobstreet, Jcbnext is now in net cash position. Therefore, it is straightforward to use its asset value as the baseline in valuation.

If Jcbnext was to liquidate or reduce capital, shareholders should receive a cash return of RM2.26/share versus its stock price RM1.78/share as at 15 Dec 2017.

That means Jcbnext is currently trading at 0.79x Price/Net Current Asset Value. Present market price is desirable for shares buy back.

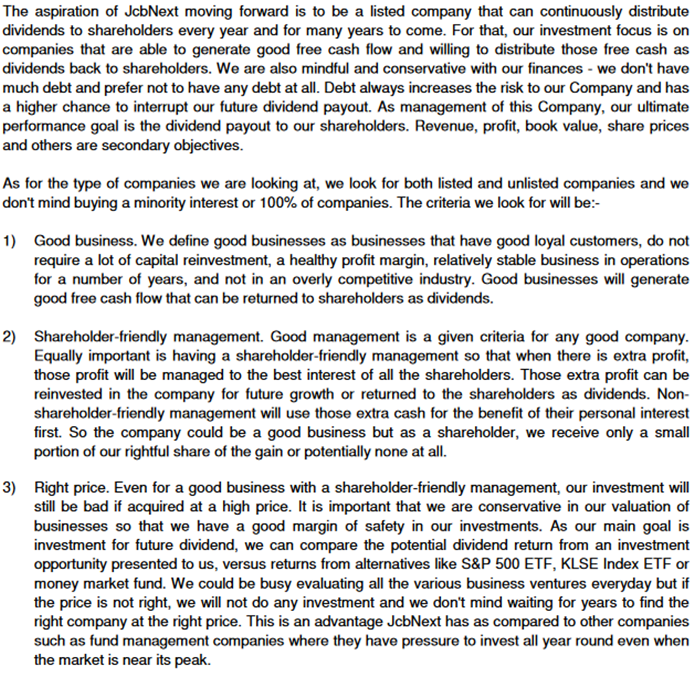

Moving forward, Jcbnext will wait for its perfect pitch.

While there are more companies and events like these 2 cases (Latitud and Jcbnext), investors should be aware that there is a buyer and a seller behind every transaction.

Your generosity to sell cheap might become an investing opportunity for a patient investor. You are encouraged to revisit your initial investment thesis of a particular stock prior to any sale.

So when do we sell?

That is a separate, but important issue. I leave that as an open-ended question, and would like to hear your intelligent view.

http://valueveins.blogspot.my/2017/12/you-sell-who-buys.html