POHUAT (7088) - 冷眼心水股: 包發 Record profit year in the making!

Poh Huat Resources Holdings Bhd TP: RM2.08 (+35.1%)

Record Profit Year in the Making? BUY

THIS REPORT IS STRICTLY FOR INTERNAL CIRCULATION ONLY*

Results review

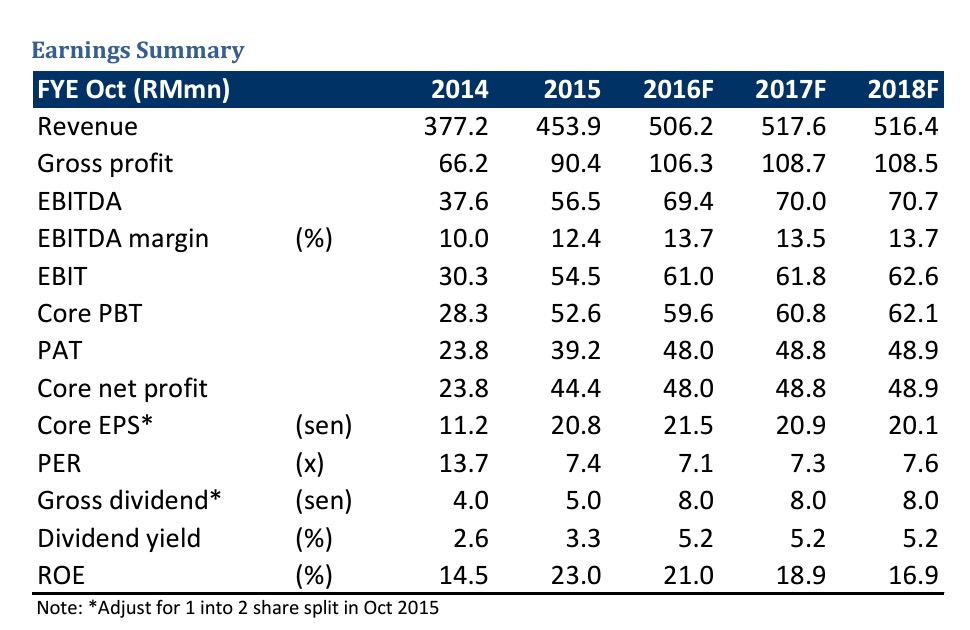

Pohuat’s 9MFY16 net profit of RM28.0mn came in within our expectation, accounting for 58.3% of our full-year estimate. Pohuat’s sales of furniture is typically stronger in 4Q of the financial year as demand picks up before year end festivities.

Pohuat has declared a third interim dividend of 2sen/share (3QFY15: 1.5sen/share), bringing 9MFY16 dividend payout to 6sen/share (9MFY15: 3sen/share).

YoY, 9MFY16 net profit jumped 19.8% to RM28.0mn as revenue increased by 22.1% to RM383.2mn, coming from both the Malaysia and Vietnam operations. Successful launch of several ranges of office furniture during the Malaysian furniture exhibition in March 2016 and sustained improved US business sentiment and employment boosted the sales of its office furniture. New bedroom products developed earlier this year increased the shipment of home furniture to the US.

However, PBT margin recorded in 3QFY16 was lower at 9.7% compared with 10.8% achieved a year ago as margin for the export sales denominated in USD normalised after sustained weakening of the Ringgit. Meanwhile, margin for operation in Vietnam were also slightly lower due to the temporary shift in the composition of mid-range products, in line with the US consumers’ preference.

QoQ, 3QFY16 revenue and net profit surged 18.0% and 156.7% respectively due to seasonality. The increase in net profit was due mainly to higher utilisation rates of its plants in the reporting quarter as in the immediate preceding quarter both of its plants in Malaysia and Vietnam were off during Chinese New Year holiday, which fell in the month of February.

Impact

In line with our in house forecast, we revise our FY17 and FY18 RM/USD assumptions to 4.125 and 4.10 respectively from 4.05. We raise our FY17 and FY18 earnings forecasts by 1.3% and 0.8% respectively.

Outlook

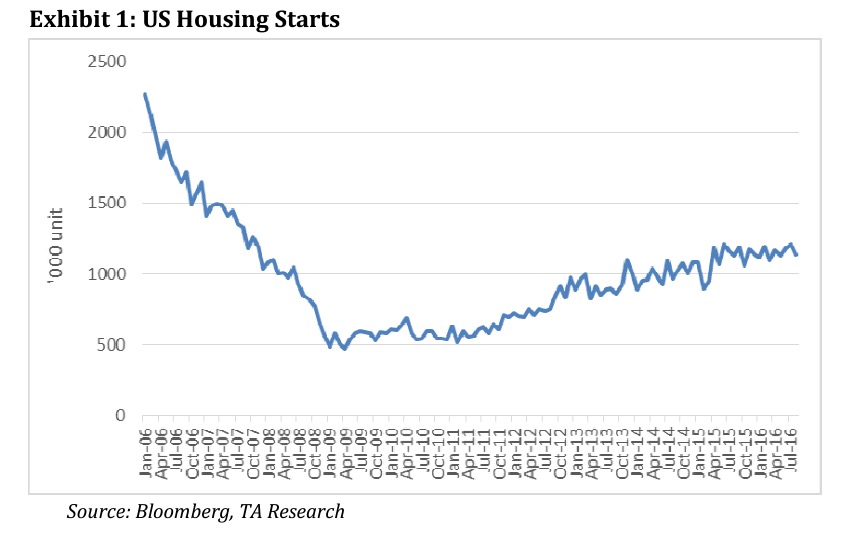

The US housing starts, which is considered to be a bellwether for the group’s furniture export to US, remain in the uptrend since hitting the bottom in early 2011. We expect Pohuat’s earnings prospects to remain robust in the foreseeable future.

Valuation

Following the revision in earnings forecasts, we raise the target price a tad higher from RM2.05 to RM2.08, based on unchanged 10x CY17 EPS. Reiterate our BUY call on POHUAT.

Source: TA Research

POHUAT (7088) - 冷眼心水股: 包發 Record profit year in the making!

http://klse.i3investor.com/blogs/MomentumInvesting88/111958.jsp