TOMYPAK recently released their Annual Report 2015 and their 2016 Q1

results. Some studies had been done on the recent Annual Report and also

the Q1 report. Previously, i had posted on TOMYPAK[1]. This will be the updated information on TOMYPAK. Let's go:

1) Fundamental Analysis:

|

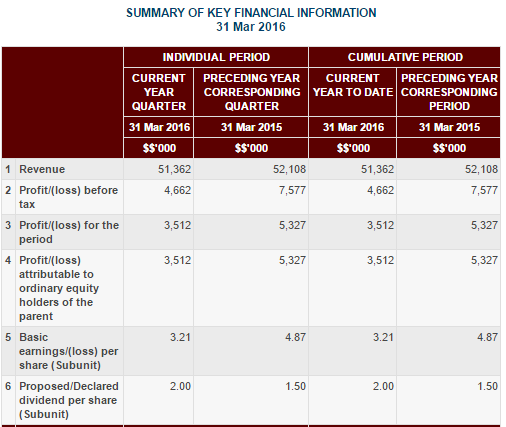

| TOMYPAK Q1 2016 Result |

Both revenue and net profit of q-o-q had decreased 1.43% and 34.07% respectively[2].

For me, the results are within expectaion, but the share price on 19

May 2016 shows another story. From the volume, a lot of shareholders are

quite disappointed with the result. Main reasons of the net profit drop

were due to:

i) Slight reduction in demand from overseas customers

ii) Increased cost of production arising from increased cost of imported raw material

iii) Higher energy and labour cost

iv) Foreign exchange volatility

|

| Impact of Foreign Exchange Volatility |

I will further elaborate on the reasons. Demand from overseas reduced 6% and 13% respectively for q-o-q and Q4 Result. Demand from locals increased 4% and reduced 4% respectively

for q-o-q and Q4 Result. The cost of imported raw material increased

due to the oil price had rebounded. Remember that the raw material of

plastic is crude oil. When the price of crude oil increased, thus the

cost production also increased. Higher energy and labour cost is because

of the new foreign worker levies charges implemented by the government[3]. As

for the foreign exchange volatility, this is something that we need to

take note for the export-oriented companies earning USD. In Q1 2015, TOMYPAK had realized gain for the foreign exchange but for this Q1, it had a realized loss of RM454k.

Although the amount is just minor, however, we need to take note of

this line item. Despite with the setbacks, TOMYPAK management is still

optimistic as the food and beverage sector remains resilient. Like my

friend say, no matter how bad the economy was, people will still eat

Maggi. In fact, more people will eat Maggi at that time, and TOMYPAK

provides plastic packaging for Maggi~ haha.

Annual Report 2015

|

| Flexible Packaging Process |

In the Annual Report 2015, Mr Chairman, Tan Sri Dato Seri Utama Arshad encouraged the shareholders to subscribe the rights issue and increase their equity participation

in the company. This corporate exercise is meant to raise sufficient

funding for TOMYPAK to complete the new plant as well as near term

operational requirements (machineries and technologies) and to serve

as a platform to reward to the supportive and loyal shareholders, as the

rights are attractively priced for the benefit of the shareholders[4]. Mr Chairman seems to be quite confident of the rights issue is not going to disappoint all the shareholders.

For 2015, TOMYPAK distributed 47.2% of its net profit as dividends,

as they still maintain their policy of distributing at least 40% of

their net profit to shareholders. Some of their upgrading and

investment efforts that were being highlighted in the Annual Report,

such as acquisition of an additional unit of advance metalizing machine

to enhance the production capabilities in producing raw material of

metalized film in Q4 2015 which boost up the production capacity from

16k metric tons to 19k metric tones per year. TOMYPAK continue to

upscale their R&D facilities, sourcing for new materials,

developing new formulations and designs and customizing, innovating

products for specific market segments.

|

| Plastic sheets for packaging |

Despite the volatile global and regional economic outlook, the soft global crude oil and commodities prices and weakening domestic currency which will eventually impact the consumer markets and Malaysia's economic performance, TOMYPAK is still confident that the demands for flexible packaging from domestic and international food and beverage sector and fast moving consumer goods will still continue to grow and expand. This is in line with the projected growth in world population and fast growing acceptance of packaged food products, all of which will lead to an increase in demand for TOMYPAK's flexible packaging from the world food and beverage manufacturers. To emphasize again, more than 90% of TOMYPAK's revenue is derived from the recession-resilient food and beverage sector.

|

| TOMYPAK providing flexible packaging to these companies |

Something to note on Mr Chairman, Tan Sri Dato' Seri Arshad bin Ayub. Aged 87, he acts as Chairman for Malayan Flour Mills Berhad (MFLOUR-3662) and Karex Berhad (KAREX-5247), Independent Non-Executive Director for Kulim (M) Berhad (KULIM-2003) and Top Glove Corporation Berhad (TOPGLOV-7113)[4].

These are all big companies. Talk about their market capitalization,

TOPGLOV (RM6,487 Mil), KULIM (RM5,639 Mil), KAREX (RM2,425 Mil), MFLOUR

(RM720 Mil) and TOMYPAK (RM282 Mil). TOMYPAK's market cap is the smallest, for me, he must had seen some long term potential prospect in TOMYPAK. Remember, all these companies are long term counters, as time goes by, they will grow. For the top 30 shareholders, not much surprise, OCBC Securities Private Limited and CIMB Principal Small Cap Fund emerges.

Rights Issue for Plant Expansion

TOMYPAK had embarked on the development of a new plant (265k square

feet) in Senai, Johor. The new plant's location is in a 10.5 acres

industrial land. Currently, it is under construction and scheduled to commence operations in Q1 2017.

Upon completion, the total area of TOMYPAK area, including existing

Tampoi plant, will be 415k square feet. More sophisticated and cost

efficient production machineries had been ordered and will undergo

testing and commissioning by the end of 2016. The details of the rights

issue had been explained in previous post, TOMYPAK- TOMY Packs His Right Path[1].

|

| Important Dates for Rights Issue |

Here are some summarized important dates to take note[5][6].

1. Ex Date (1 June 2016): If you sell your shares on or after the date, you will still be entitled for the rights issue.

2. Commencement of Trading of Rights (6 June to 10 June 2016): On

6 June 2016, TOMYPAK-OR will appear in your portfolio. If you do not

want to subscribe the rights issue, you need to sell off all the

TOMYPAK-OR. The last day is 10 June 2016.

3. Payment Period (13 June to 17 June 2016): You had subscribed for the rights issue, therefore you need to pay the amount of RM1.00 for each rights issue subscribed.

4. Announcement for subscription (27 June 2016): You will be able to know whether your subscription is successful or not. By right, there should not be any problem.

5. Listing Date of Rights (5 July 2016): TOMYPAK-WA will be listed out on this date.

Case Scenario: *The calculations might be incorrect, however i will write up on the prices once the listings had happened.

Assume, we had bought the 4,000 shares of TOMYPAK at 2.4.

On 1 June, assume the closing price of TOMYPAK is 2.80

On 2 June, TOMYPAK price will be adjusted to 2.20*. The rights issue, TOMYPAK-OR will be 1.20* even though the issue price is 1.00. Our TOMYPAK volume is still 4,000 shares, but price will be adjusted to 1.93*.

We will have 2,000 shares of TOMYPAK-OR. If we want to subscribe to the

rights issue (1.00 per Rights Share), we need to pay RM2,000 before 17

June 2016.

On 5 July, all the shareholders will have their TOMYPAK-WA in their CDS account. We will be entitled with 2,000 shares of TOMYPAK-WA.

To recap, my calculations might not be correct, i will monitor it for

learning purposes and update once all the listings had happened.

2) Technical Analysis:

Summary:

|

| TOMYPAK Daily Chart |

When the Q Result is announced on 18 May 2016, on the next day, the chart gap down however was well supported by the lower Bollinger Band. The price was pushed up and formed a hammer.

For me, this hammer is not a powerful hammer as it did not happened in

the downtrend. It was not a reversal either. Just someone is buying

whilst other are panicly selling their TOMYPAK. On 20 May 2016, there is

a big bullish engulfing which covers the gap. However, i expect within next few days, the price might fall down as the volume is not sufficient. With a resistance at 2.55, the chart is forming a cup with handle,

waiting for break out. But as i mentioned, the volume seems not

adequate enough to breakout. However, if the chart can stay above 2.55

for 3-5 days, i can assume 2.55 to be a strong support. The support is

strong at 2.40, as it rebounded when it breach 2.40. The next resistance

will be 2.70.

TOMYPAK should be a mid to long term stock as the business model

is recession proof. The company is generous at giving dividends and

maintaining its dividend policy of 40%. Even though they have a tough

start in their first quarter, but i am expecting most companies will be

announcing not-up-to-expectations results, in another word,

disappointing results. You can always click on the link to refer to my

previous post on TOMYPAK.

- Recent Q1 is poor if compared to the last

quarter and last preceding quarter due to lower demands from

international market, increased raw material cost and labour fee, and

also foreign exchange volatility.

- Ex date for dividend 2 sen on 31 May 2016.

- Rights Issue for business expansion had been confirmed. The ex-date is on 1 June 2016.- Ex date for dividend 2 sen on 31 May 2016.

- Business expansion plans include focus

on improvements on its existing production capacities through

investments into new and more advanced production machineries for higher

output, automation and better efficiencies. The new plant is scheduled

to commence operation on Q1 2017.

- Mr Chairman, Tan Sri Dato Seri Utama Arshad had urged all the shareholders to subscribe the rights issue as the rights are attractively priced for the benefit of the shareholders. Mr Chairman is also present in TOPGLOV, KULIM, KAREX and MFLOUR. Considering his ROI, i guess it is very good for long term investing.

- From technical point of view, TOMYPAK seems to form cup with handle but the volume is not adequate to break out. The resistances are 2.55 and 2.70 while the support is at 2.40.

- Respect the cut loss point very much during the volatile market.

- Mr Chairman, Tan Sri Dato Seri Utama Arshad had urged all the shareholders to subscribe the rights issue as the rights are attractively priced for the benefit of the shareholders. Mr Chairman is also present in TOPGLOV, KULIM, KAREX and MFLOUR. Considering his ROI, i guess it is very good for long term investing.

- From technical point of view, TOMYPAK seems to form cup with handle but the volume is not adequate to break out. The resistances are 2.55 and 2.70 while the support is at 2.40.

- Respect the cut loss point very much during the volatile market.

Gainvestor mid term TP: 3.00 (after rights issue)

Let's Ride the Wind and Gainvest

Gainvestor 10sai

22 May 2016

7.30pm

Sources:

[1]: TOMYPAK - TOMY Packs His Right Path: http://gainvestor10sai.blogspot.my/2016/03/tomypak-tomy-packs-his-right-path.html

[2]: Q1 2016 Result: http://www.bursamalaysia.com/market/listed-companies/company-announcements/5095849

[3]: New foreign worker levies for Peninsular Malaysia effective today: http://www.thestar.com.my/news/nation/2016/03/18/foreign-worker-levies-penisular-malaysia/

[4]: Annual Report 2015

[5]: http://www.bursamalaysia.com/market/listed-companies/company-announcements/5098501

[6]: http://www.bursamalaysia.com/market/listed-companies/company-announcements/5098469

[2]: Q1 2016 Result: http://www.bursamalaysia.com/market/listed-companies/company-announcements/5095849

[3]: New foreign worker levies for Peninsular Malaysia effective today: http://www.thestar.com.my/news/nation/2016/03/18/foreign-worker-levies-penisular-malaysia/

[4]: Annual Report 2015

[5]: http://www.bursamalaysia.com/market/listed-companies/company-announcements/5098501

[6]: http://www.bursamalaysia.com/market/listed-companies/company-announcements/5098469

TOMYPAK (7285) - TOMYPAK - Rights Issue Underway

http://gainvestor10sai.blogspot.my/2016/05/tomypak-rights-issue-underway.html