OLDTOWN (5201)

OldTown is a regional cafe chain operator (F&B) and an established

beverage manufacturer (FMCG) based in Malaysia. As at FY15, the group

derived 55% of its revenue from F&B and 45% from FMCG.

F&B stocks have been garnering investors’ interest due to their

resilient nature, export exposure and also falling commodity prices.

Besides, F&B remain challenging due to the dampened consumer

sentiment post-GST implementation and series of administered price

hikes.

As at 2QFY16, there are 242 outlets operating in total. Throughout

1HFY16 there were 11 new openings and 16 closures and renovations. Of

the 242 stores 87% are located in Malaysia.

PBT jumped 21% q-o-q on the back improved share of profits from its

Singapore café outlets despite a marginal increase of 1% in revenues

qoq. There are currently 9 café outlets in Singapore with 2 more slated

to commence operations by end FY16.

The groups’ promotional activities have centered on value inducing

purchases such as their “RM10 value meals” promotions. Moving into

2HFY16, its value inducing pricing strategy and discounting is expected

to persist to attract customers. YTD revenues per outlet are down circa

12% on a yoy basis.

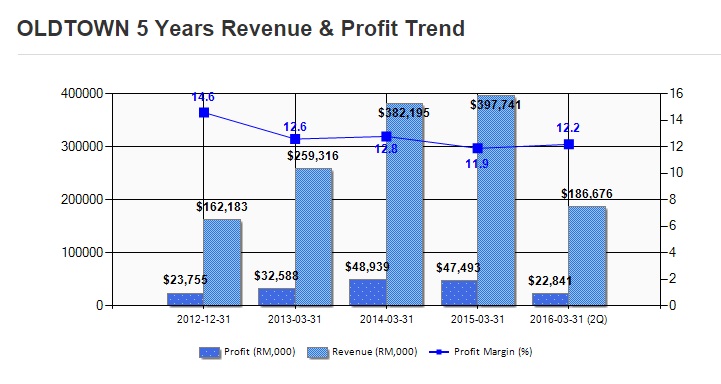

1HFY16 revenues grew by 11.1% on the back of double digit growth in

modern trade in the 3 key markets which are M'sia, HK & S'pore.

Taiwan has emerged as another key market for the group in recent times.

PBT grew by 17%, aided by the stronger USD. Recall that their exports

are priced in USD.

Its exports to China registered a slight decline y-o-y on the back of

their distribution rationalization; however this is not reflexive of a

drop in demand for OTWC products. Walmart has been signed on as a key

player in their modern trade channel. Walmart has 450 stores across

China.

Margins would be supported by prudent cost management, which saw

packaging materials cost decrease by 8% y-o-y, meanwhile the full

commissioning of the automation of their packaging line end 3QFY16 will

reduce direct labor expenses in the long run.

Besides, its strong balance sheet position with net cash of RM151.0m

(32.6 sen/share) provide further room for higher dividend pay-out which

estimated at 6.0 sen/share and 6.5/share (yield: 4.3% & 4.6%) for

FY16E & FY17E, respectively, based on a conservative pay-out ratio

of c.52% vs 4-year’s average of 55%. Potential dividend yield might

exceed 5% if the Group pays 60% of its earnings.

Kenanga Target price given RM 1.76

Disclaimer:

All posts and documents submitted in this blog are solely for open discussion and education purposes only. All recommendations and opinion provided are solely for your consideration only and you should exercise your own judgment in forming your own investment decision(s). Please also be informed that equity investment is risky and we recommend you to conduct sufficient searches for information in addition to referring our recommendations and/or opinion herein, prior to making an investment decision.

You should take full responsibility of your investment decision(s) and we accept no liability whatsoever for any direct or consequential loss arising from any use of our recommendations and/or opinion provided herein or any solicitations of an offer to buy or sell any securities. Comments and opinions forwarded/provided by members/followers of this blog do not belong to the Admin and we take no responsibility of such.

OLDTOWN (5201) - OLDTOWN - Aroma of Good Times

http://fatta888.blogspot.my/2015/12/oldtown-aroma-of-good-times.html