1.0 Investment Summary

Landmark

Bhd (Landmark), the master developer of Treasure Bay Bintan(TBB), may

see its share price enjoy better valuation soon with the opening of

Phase 1 in Q2 this year. TBB is an ambitious RM11.6-billion waterfront

resort city development project in Bintan, Indonesia that could

potentially become the next island-and-beach tourism hotspot in SEA,

just like Phuket and Bali. The coming opening and any news on new

partnerships or SPAs signed may catalyze the stock price re-valuation. I

am giving a Buy rating on Landmark with SOP Target Price at RM2.74 (97%

upside potential) based on positive long-term outlooks of TBB as

below:

|

| TBB's Master Plan |

Strategic proximity to Singapore - next to Bintan Bandar Telani Ferry Terminal, it is just 45-min ferry ride away from Singapore. This geographic advantage make TBB a convenient destination to Singapore's 15 million annual visitors, 5.4m population as well as 54m air passengers. Bintan is also set to attract more international visitors with the opening of new Bintan International Airport in 2016, which is 25-min drive away from TBB. Besides that, there have been increasing Indonesia-Singapore cooperation on the promotion and development of Bintan, which make Bintan a special economic zones (SEZ) that receives investor-friendly policies that help attracting FDI.

|

| Source: williamfives.com |

Emerging tourism hotspot with ambitious development - Bintan share various tourism attractions, like clean-white-sand beaches with clear ocean water, tropicana weather and forests as well as its unique architecture and cultural value, with peers such as Langkawi Island, Phuket and Bali. Bintan is currently at the early-stage of various long-term and large-scale master-planned development, most notably are the 1300-hectares Lagoi Bay development by Gallant Venture Ltd of Singapore as well as TBB by Landmark. Compared to its peers, which are in more mature stage, BI offer investors an earlier opportunity to invest in this emerging development.

|

| Many developments are happening in Bintan Island |

Bintan Resorts

attracted almost half a million tourists in 2012. With more hotels rooms

available, it should grow at a faster rate moving forward.

|

| Source: Lagoi Bay Investment Guide |

Fast-growing Tourism Industry in Indonesia - Based on World Travel and Tourism Concil (WTCC), Indonesia's Tourism GDP is expected to grow by 5.3% pa from 2014's IDR325 trillion to IRD581 tn by 2025. Besides that, they forecast international tourist arrival to Indonesia and their expenditure to grow by 5.5% pa in the next 10 years. This growth will attract international investors interest to invest in the industry and hence, Bintan should be one of the beneficial of this trend. WTCC also sees the industry's capital investment to grow at 7.1% pa over the next 10 years. With this positive investment trend, TBB have great opportunity to attract more investment to their development project through various methods such as land sales, partnership with hotel operators and build-and-sales properties.

|

| Source: WTTC |

The Buy Rating is also supported by:

TBB is entering fast-growth phase - TBB has finished the long gestation stage as a greenfield site previously and now is ready to enter the next phase of development. Started in 2006 with the land acquisition, TBB has been in gestation stage since then with few master plan revision and delay in development especially due to Global Financial Crisis in 2008. However, I believe TBB is entering a fast-growth phase soon with the opening of Phase 1 in Q2 2015.

|

| Source: http://thedevelopmentadvisor.com/ |

Large discount to RNAV provide massive revaluation potential - Using 11 Apr 2015's closing price of RM1.37, Landmark is currently trading at 73% discount to my RNAV (RM5.15) or 64% discount to its Book Value(BV) of RM3.68. Landmark has been trading at steep discount to its BV in at least the past 5 years, which is not unreasonable as TBB was still a greenfield project in the past where investment risk and uncertainties were still high. However, with the opening of Phase 1 in this quarter, TBB's prospect will become more visible. Any announcement on new partnership, investment or S&P signed will catalyze the stock revaluation. One of the possible example is that following the announcement of CYB development in Jun 2014, Landmark share price surge over 40% in the following month, Aug. Though the share price has since retreated and the surge may just a market speculation, any more positive announcements in the future may sparks more long-term investors' interest.

Based on a Sector Update on Property Developers by Kenanga Research on Apr 2015, the sector is currently trading at an Overall Sector Average Discount of 50% to Kenanga's FD RNAV. The huge discount on the sector is based on pessimistic outlook on Malaysia's property market. However, Landmark beg to differ the sector average and should be trading at a lower discount because it's a very unique investment opportunity. Landmark is perhaps the only stock that provide direct opportunity to invest in such a large scale resort city project in Indonesia, compared to the many property developers in Malaysia competing in the same landscape. The next closer alternative is Gallant Venture Ltd(GV), the master-developer of Lagoi Bay Bintan, in Singapore. However, GV is in diversified business, Landmrk is a more straight-forward investment as Landmark other business (besides TBB) provide about 10% of its RNAV. Hence, my 40% discount to RNAV is reasonable.

Gaming license a possible future wildcard - Last but not least, Landmark, a 30%-Genting Bhd owned company, could potentially opened the first casino in TBB. In 2008, Landmark has received consent from Indonesia authority to operate gaming business in TBB. However, there are no much development after that and starting a gaming business in a country that do not have casino before can be challenging from politic and social point-of-view. Hence, it is safer not to incorporate this development into the valuation, but it can be a wildcard in the future.

2.0 Business Background

Landmark listed in Bursa Malaysia (known as KLSE that time) in 1990, is in the business of hospitality and property development. Prior to 2006, the company was involved in development of (1)3 hotels in Labuan and Langkawi (2) Bandar Baru Wangsa Maju township (through equity interest in MSL Properties SB, a subsidiary of IJM Corp) and (3) the new township of Cyberjaya (through a JV with Setia Haruman SB). The company also previously on Sungai Wang Plaza as their investment. Since 2006, the Group re-positioned itself to focus on the TBB project. The new focus make Landmark to dispose most non-core businesses.

Currently, Landmark have businesses in these 3 areas:

1) TBB

2) The Andaman, a 170-room luxury hotel in Langkawi

3) The development of Bandar Baru Wangsa Maju through 20% + 1 equity interest in MSL

The Andaman has undergone some major refurbishment in 2013, which caused significant drop in revenue and loss-making in FY2013. After that, the strategy start to bear fruits with its revenue raise to its 5-years-high due to better room-selling-price and occupancy rate.

Shareholding structure

Genting Bhd has on 2008 acquired 30% share in Landmark Bhd at share

price of around RM2.00 per share (44% above current price) and has since

become the largest shareholder of the company.

3.0 TBB

The latest known project GDV is at RM11.27 bil based on a news by TheEdge in 2014.

TBB Information:

- 45 min ferry ride from Singapore

- 75 mins car ride from Kijang Airport. 25mins away from new Bintan International Airport to be opened in end 2016

- To be fully developed in 20 years

Phase 1:

- 90 hectare with DGV of RM2.1bil

- Featuring Cystal Lagoon, 6.3-ha man-made lagoon with trademarked technology of Crystal Lagoon, which help made crystal clear inland lagoon (more info: http://www.urban-beaches.com)

- A center attraction for leisure, water activities and with surrounding F&B and retail outlets

- 1,700 room keys

- 8 hotels and a wellness resort by Canyon Ranch

Phase 2: (ecpected to be launched in the next 3 years

- Launching and selling of Ring Resorts, Waterfront villas, Marina Private Residences

- Private Mangrove Park

- Commercial areas

- Second wellness resort by Chiva-Som

Phase 3:

- Town centre, Hospital, Education Campus, Retail, Residences

|

| Current site condition Source: Project Facebook Site |

|

| Various hotel/resorts in Bintan |

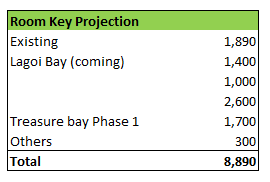

Number of room keys are booming in the coming years and may reach 8890 room keys by 2018.

With Lagoi Bay

expected to have 5000 room keys before 2020 and 1700 room keys in TBB

Phase 1, hotel rooms is expected to experience oversupply condition in

the early stage.

Possible source of return - TBB may generate return via the following means:

- Sales of

hotel/resort development lands to hospitality investor or operator. This

will generate immediate large amount of return.

- Lease of land for hotel/resort development; to generate recurring income

- Operate retail, F&B outlets and leisure activities

- Develop and own hotel to be operated by reputable hotel operators

- Build and operate hotel

- Build-to-sales villas, residential and commercial units

The choice of operandi modius will affect Landmark future income structure.

4.0 Finance

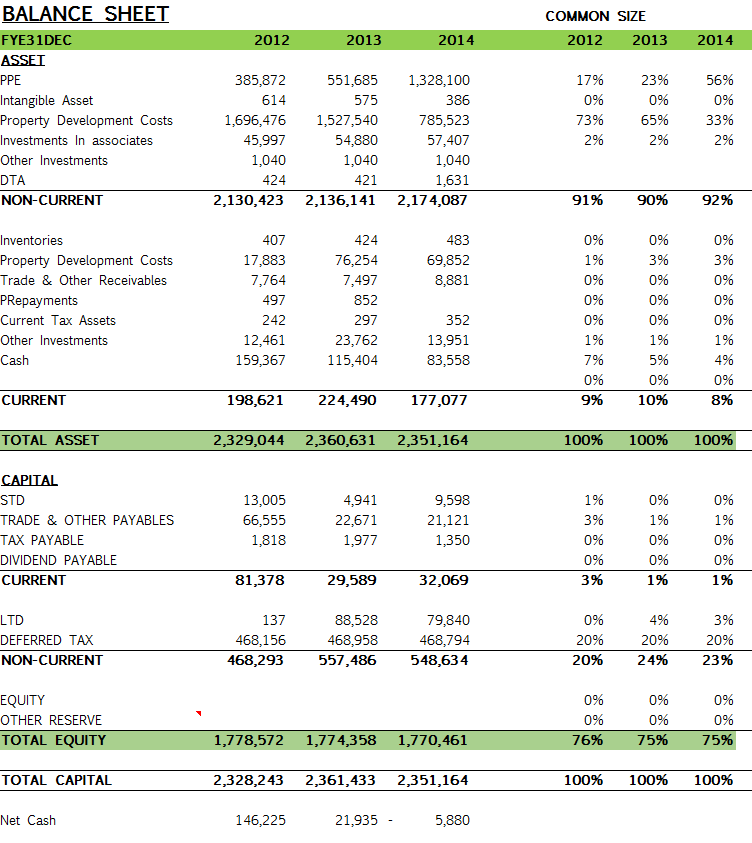

Landmark's

Asset largely dominated by TBB's land which, together with Property

Development Costs, were about RM2.0 bil. Net Cash dropped from RM146mil 2

years ago to current net debt of RM6mil. Net Gearing is nil..

Though the

hospitality (The Andaman) and Property development business are

profitable, Landmark has been loss making in the past due to high

operating cost in developing the TBB land.

5.0 Risks

Unable to secure new partnership or receive new investment in the medium term or retreat of agreed investment - this will create doubt on the prospect of TBB. However, involvement Canyon Ranch and Chiva-Som give an early indication of TBB's ability to attract investment.

Drop in investment to Indonesia and the tourism industry - any negative change in future growth outlook may affect foreign investment. Rising cost of capital due to Fed rate hike and strengthening of USD against IRD will also discourage investment. However, this can partially offset by the easing monetary condition in Europe, Japan and possibly China.

Oversupply of hotel rooms delay future new investment or Phase 2 - large amount of hotel rooms are going to be developed in the next 2-3 years on expectation of rapid-rising of visitors. If growth in visitors amount unable to match with growth in hotel room supply, overcapacity will pressure occupancy rate and selling price and may eventually slow down new investment. However, hotel investor normally have long-term investment period and is expecting to make investment decision based on their confidence on the longer-term outlook.

Unfavorable global economy condition - the TBB project was previously delayed due to 2008 Global Financial Crisis. If global recession occur again before any significant development taken place, it will seriously affect investment.

6.0 Valuation

5.0 Risks

Unable to secure new partnership or receive new investment in the medium term or retreat of agreed investment - this will create doubt on the prospect of TBB. However, involvement Canyon Ranch and Chiva-Som give an early indication of TBB's ability to attract investment.

Drop in investment to Indonesia and the tourism industry - any negative change in future growth outlook may affect foreign investment. Rising cost of capital due to Fed rate hike and strengthening of USD against IRD will also discourage investment. However, this can partially offset by the easing monetary condition in Europe, Japan and possibly China.

Oversupply of hotel rooms delay future new investment or Phase 2 - large amount of hotel rooms are going to be developed in the next 2-3 years on expectation of rapid-rising of visitors. If growth in visitors amount unable to match with growth in hotel room supply, overcapacity will pressure occupancy rate and selling price and may eventually slow down new investment. However, hotel investor normally have long-term investment period and is expecting to make investment decision based on their confidence on the longer-term outlook.

Unfavorable global economy condition - the TBB project was previously delayed due to 2008 Global Financial Crisis. If global recession occur again before any significant development taken place, it will seriously affect investment.

6.0 Valuation

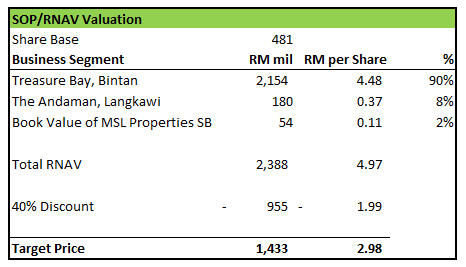

My estimated NPV of TBB is at RM2.15 bil which is reasonable compared to previous valuation done by valuer. The TBB's land was in 2008 valued by valuer using Land Development/Residual Method, which take into consideration of TBB's master development plan, and the Investment Value was at RM1.87 bil. Considering the project's GDV has since increased 17% to RM11.27 bil (from 9.7 bil during consideration for land valuation) and cost of capital has been lower significantly worldwide after the Global Financial Crisis, my NPV estimate, which is 15% higher than previous valuation, is justifiable.

40% discount to RNAV is given since TBB is at its early stage of development. The current market discount is at 73%, which is very low as I expect more positive news flow coming in the next 12 months, especially after opening of Phase 1 in Q2 2014.

Based on Kenanga's report on Property Sector, the sector's stocks is currently trading at overall average discount of 50% of their FD RNAV. Landmark beg to differ as it's in resort city development project in Indonesia compared to the listed property developers that are mostly involved residential and commercial projects in a competitive environment.

To incorporate the possibility that no new development (status quo) or partnership announcement in the next 12 months, I further adjust my TP based on Probability-weighted on these 2 possible scenarios.

In conclusion, I give Landmark a Buy rating with TP of RM2.74, which provide 97% upside potential.

7.0 Summary

i) Buy rating on Landmrk with TP at RM2.74 based on 40% discount to RNAV and 15% probability of no new development

ii) Positive long-term outlook on TBB due to its proximity to Singapore, growth in no. of

visitors and tourism industry as well as rising investment in Indonesia Tourism

iii) Expecting revaluation for Landmark share price catalyzed by opening of TBB's Phase 1 and potential announcement of new partnership

iii) Despite current depressed valuation in Malaysia property sector stocks, Landmark offer unique investment opportunity to large-scale long-term resort city development in Indonesia. Hence, a niche.

iv) The risk are a) no major development in the next 12 months or retreat of agreed development b) drop in investment in Tourism industry c) oversupply of hotel rooms d) unfavorable global economic condition

8.0 Technical Analysis

Landmrk is in long, medium and short term uptrend based on MA. Price Momemtum is bullish with RSI and Stochastic above 50% in the past 3 months with gradually rising average Volume. Immedite Resistance has turned to Support at RM1.38. The next 2 resistance is at RM1.55 and RM1.66.

9.0 Appendix

TP Sensitivity Analysis

http://bullandbearresearch.blogspot.com

{kind=link}